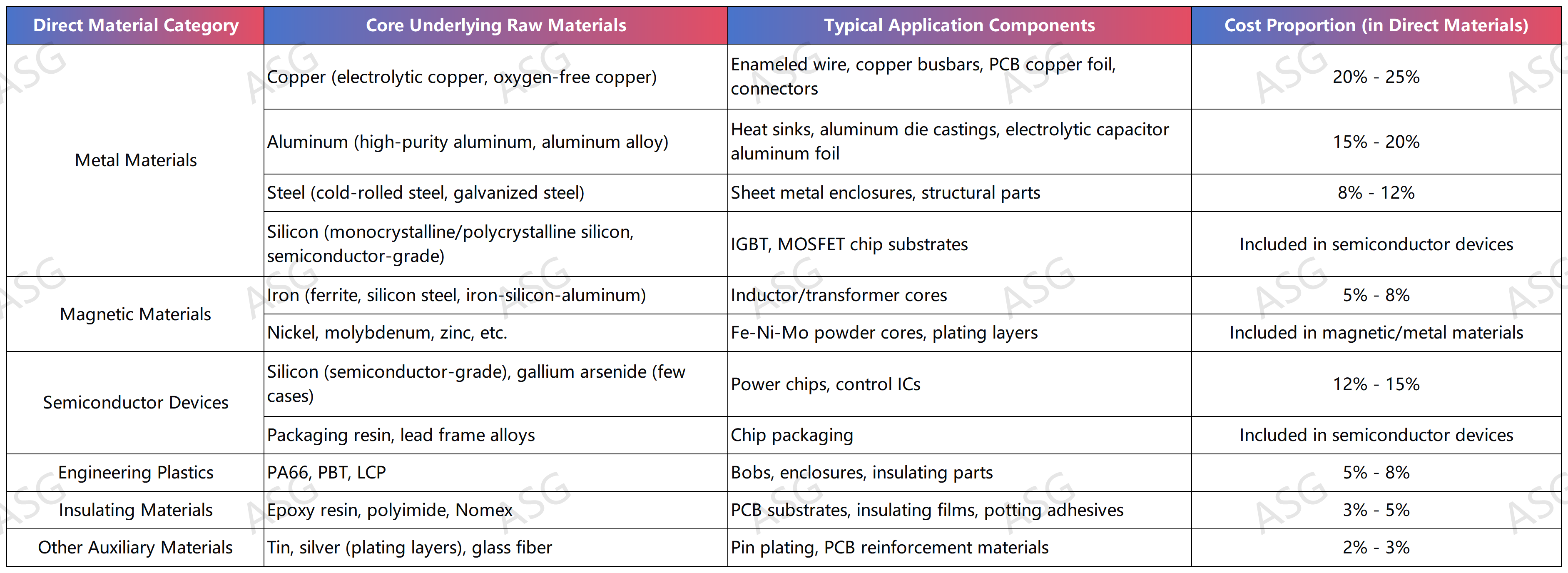

The Cost Breakdown of Direct Materials for Energy Storage Inverters

Energy storage inverters are core components that connect renewable energy systems to power grids, and their direct material costs account for approximately 84% of the total production cost. The following is a detailed breakdown of the underlying raw materials of direct materials, their typical applications, and their corresponding cost proportions within direct materials, based on industry public data and inverter cost structure calculations.

Key Notes

- Cost Proportion Scope: Based on the premise that direct material costs account for 84% of the total inverter cost, the above proportions are relative to direct materials, not the total production cost.

- Core Proportion Ranking: Metal materials (copper, aluminum, steel) account for approximately 43% - 57% of direct materials, making them the main part of direct material costs. Semiconductor devices and magnetic materials together account for 17% - 23%, which are the core determinants of inverter performance. Auxiliary materials such as plastics and insulating materials account for 10% - 16% in total.

- Factors Affecting Proportion Differences: Power rating (residential 3kW / commercial & industrial 50kW), topological structure (centralized / string), and technical route (high-voltage / low-voltage) will lead to fluctuations in cost proportions. For example, high-voltage inverters may have higher semiconductor costs.

To sum up,From a bulk commodity perspective, iron, aluminum, copper, and silicon account for 20%, 20%, 25%, and 15% of the direct material costs of inverters respectively.

Therefore, the price increases of these four raw materials will affect 80% of the direct material costs of inverters.

As of now, data shows that on January 13, China's domestic aluminum price hit a historic breakthrough. The price of the most active SHFE aluminum contract topped the 25,000 yuan/ton mark for the first time, setting a record high. Following the SHFE copper price breaking through 100,000 yuan/ton and continuously renewing records, aluminum has become another strong non-ferrous futures variety to hit an all-time high after copper.

From a fundamental perspective, Liu Yunyan, an electrolytic aluminum analyst at Zhuochuang Information, told reporters from Securities Daily that the aluminum price rally is mainly driven by three factors. First, the expected tightening on the supply side underpins the price increase, with uncertainties surrounding future supply expectations pushing up aluminum prices both domestically and internationally. Second, positive shifts in the macroeconomic environment provide certain support for aluminum prices; rising market risk aversion and the transmission of energy cost fluctuations to aluminum price expectations have reinforced bullish sentiment. Third, copper and aluminum are mutually substitutable in multiple sectors such as home appliances and wires/cables. The copper price surging past the 100,000 yuan/ton threshold has triggered a catch-up rally in aluminum prices.

SHFE Aluminum Weekly Chart

SHFE Copper Weekly Chart

Looking ahead, industry analysts believe that driven by the sustained growth in rigid demand from emerging industries such as new energy vehicles, computing power, and energy storage, the demand for aluminum, copper, and similar commodities is expected to grow steadily. Meanwhile, non-ferrous metals, as high-quality assets, will gain greater favor in the market.